DP World does not look like a publicly visible champion. The company has been private since 2020. It does not run a glossy investor relations roadshow. Its CEO speaks rarely outside industry forums. And yet, every time a container ship leaves Shanghai bound for Rotterdam, every time Saudi crude products move toward East Africa, every time Indian textiles reach the United Kingdom, the odds are that DP World terminals are doing some part of the work. The Dubai-based operator runs more than 80 marine terminals across 60 countries, handles more than 90 million TEU of containers a year, and sits at the centre of one of the most strategically valuable logistics networks on the planet.

This article is the 2026 inside guide to that empire. It walks through how the company was built, who runs it, where its ports actually sit, how the financial engine works, and what is changing in 2026 as Red Sea disruption, Africa expansion, and digital logistics platforms reshape global trade flows. For analysts, regional observers, and anyone trying to understand why Dubai’s free zone economy still functions like a pressure valve for global trade, DP World is the institution to study first.

From Dubai Ports Authority to a Global Operator

DP World as a corporate entity is younger than many people assume. It was formed only in September 2005, through the merger of Dubai Ports Authority — which had operated Mina Rashid since 1972 and Jebel Ali since 1979 — with Dubai Ports International, the international acquisition vehicle that the Authority had spun out earlier in the 2000s to chase deals abroad. The merger was driven by a single strategic insight from Sultan Ahmed Bin Sulayem: Dubai’s value as a port was no longer captured by the volume of containers physically passing through Jebel Ali. It was captured by Dubai’s ability to operate the Jebel Ali model elsewhere.

The proof case arrived almost immediately. In 2006, the new DP World acquired the British operator P&O for $6.85 billion in what was, at the time, one of the largest cross-border port deals ever signed. The transaction was politically explosive in the United States, where six P&O-operated US terminals became the focus of a national security debate that ultimately forced DP World to sell those specific assets to AIG. Outside the United States, however, the P&O deal handed the new Dubai operator a global terminal portfolio overnight, including container terminals in Antwerp, Southampton, and Tilbury, plus operations across Asia and Australia.

From that base, the company expanded almost continuously. The 2007 Nasdaq Dubai IPO raised approximately $4.96 billion, valuing the firm at around $25 billion at issue, and gave Bin Sulayem the public balance sheet to keep buying. Acquisitions of Drydocks World in 2020, the Syncreon contract logistics business in 2019, the Imperial Logistics group of South Africa in 2022, and a series of African and Latin American greenfield concessions added scale and breadth. By 2024, DP World had repositioned itself from a port operator into what the company calls an “end-to-end supply-chain solutions provider” — a phrase that sounds like marketing but reflects a real shift away from pure terminal handling toward warehousing, freight forwarding, customs, and trade-finance integration.

The Ownership Structure

Understanding DP World’s place in the Dubai economy requires understanding the holding structure above it. The company is wholly owned by Port and Free Zone World FZE, which sits inside Dubai World, which in turn reports up to two parallel apex holdings of the Dubai government: the Investment Corporation of Dubai (ICD) and the Ports, Customs and Free Zone Corporation (PCFC). PCFC also controls the related Jafza free zone, the Dubai Customs apparatus, and several adjacent logistics assets. The dual-apex structure dates back to the 2008-2010 Dubai debt restructuring when Dubai World required a complex realignment of its assets, and it has not been simplified since.

Sultan Bin Sulayem chairs both DP World and PCFC. That overlap is not accidental — it is the explicit governance design that allows DP World to coordinate seamlessly with Jebel Ali Free Zone, with Dubai Customs, and with the broader Dubai logistics-trade machine. For comparison, Maersk, PSA International, and Hutchison Ports operate as standalone commercial entities with arms-length relationships to their host states. DP World, like China’s COSCO Shipping Ports, sits inside an integrated state-trade complex. That integration is part of why Jebel Ali handles transshipment volumes that pure-commercial competitors cannot match.

The Global Footprint Map

As of the start of 2026, DP World’s operating footprint covers 82 marine terminals, 51 rail or inland terminals, and several dozen logistics parks and free zones across more than 60 countries. The geographic spread is meaningful because it gives the company simultaneous exposure to nearly every major shipping corridor: Asia-Europe via Suez, the Red Sea-Indian Ocean Africa loop, the trans-Atlantic, and intra-Asia. Few competitors have this breadth — APM Terminals (Maersk’s affiliate) comes closest, while PSA International and Hutchison Ports are more concentrated in Asia.

| Region | Marine terminals | Approx. annual TEU (millions) | Strategic role |

|---|---|---|---|

| Middle East and South Asia | 14 | 32 | Anchor region, Jebel Ali transshipment |

| Europe | 15 | 14 | Asia-Europe gateway terminals |

| Asia Pacific | 11 | 17 | China, India, Vietnam linkages |

| Sub-Saharan Africa | 12 | 9 | Highest-growth corridor |

| Americas | 13 | 11 | Latin America focus, plus Vancouver |

| Australia and New Zealand | 5 | 3 | Stable mature handles |

| Other (Russia, Caucasus, etc.) | 12 | 4 | Smaller niche operations |

| Total | 82 | ~90 | Global integrated network |

The middle-east and south-asia cluster is decisively the largest. That is partly because Jebel Ali alone handles 14-15 million TEU per year and runs at roughly 22 million TEU of nameplate capacity. The complex is not just a port — it is the world’s largest man-made harbour, integrated directly with Dubai’s rail-road network and the adjoining 57-square-kilometre Jebel Ali Free Zone. Beyond Jebel Ali, the cluster includes Karachi (Pakistan), Sokhna (Egypt), Mumbai-Pipavav, Cochin Vallarpadam, and the Doraleh terminal in Djibouti.

Jebel Ali: The Anchor

Jebel Ali deserves a section on its own because no other DP World asset comes close in strategic value. The port was opened in 1979 and handled its first container ship in 1983. By the early 2000s it had displaced Aden as the leading transshipment hub on the Asia-Europe corridor. By 2024 it had reached more than 22 million TEU of nameplate capacity across four container terminals and 67 quay cranes, with throughput typically running at 14-15 million TEU per year.

The port serves multiple roles simultaneously. It is the export gateway for the Northern Emirates, including Sharjah and Dubai-based manufacturing. It is the import gateway for the entire UAE consumer economy. And critically, it is a transshipment hub — meaning roughly half of the containers entering the port leave again on a different vessel without their cargo touching UAE soil. Transshipment volumes are commercially valuable because they generate handling fees on the way in and on the way out, but they require operational scale and reliability that few ports can deliver.

The free-zone integration matters here. Jebel Ali Free Zone sits adjacent to the port and houses more than 9,500 companies, ranging from logistics multinationals to manufacturing operations to professional services. A container moving from a ship to a Jafza warehouse can be cleared in hours rather than days. That speed is part of why so many regional distributors have chosen Jebel Ali over alternative ports such as Khalifa (Abu Dhabi), Salalah (Oman), or Sohar (Oman). For deeper context on why this matters for the Dubai economy specifically, see our analysis of Dubai free zone vs mainland structures.

Africa: The Strategic Bet

If Jebel Ali is the anchor, Africa is the strategic frontier. DP World now operates marine terminals in Senegal (Dakar), Mozambique (Maputo), South Africa (Cape Town and Durban via Imperial Logistics), Rwanda (Kigali Logistics Platform), Egypt (Sokhna and Sokhna 2), Algeria (Algiers and Djen-Djen), Somaliland (Berbera), and Djibouti (Doraleh, with ongoing legal disputes). Add the inland logistics network that came with the 2022 Imperial Logistics acquisition and DP World now arguably has the deepest single-operator footprint on the African continent of any global port operator.

The bet is that African import-export volumes will outpace the rest of the world for the next decade. Sub-Saharan Africa’s container trade grew at roughly 6.4 percent compound annual growth from 2018 to 2024, against 3.1 percent globally, according to Reuters shipping coverage. Population growth, urbanisation, and the African Continental Free Trade Area implementation are projected to lift this rate further through 2030. DP World’s challenge is to remain ahead of competitors — particularly China COSCO and Bollore-MSC (now under MSC ownership) — that are pursuing the same continent.

The most consequential African investment is at Berbera in Somaliland, where DP World has spent more than $440 million since 2017 to expand the port from a 4 metre container handling depth to a deep-water 17 metre terminal capable of receiving Panamax and post-Panamax vessels. Berbera positions DP World as a counterweight to the Chinese-operated Doraleh facility in neighbouring Djibouti, where DP World was forcibly removed by Djiboutian authorities in 2018 in a contractual dispute that remains in international arbitration. The Doraleh dispute is one of the few public reminders that even DP World’s operational reliability has limits when host-state politics turn hostile.

India: The Other Growth Engine

India sits alongside Africa in DP World’s strategic top tier. The company operates Mumbai-Pipavav (50 percent stake plus operating control), Mundra (operating concession), Cochin Vallarpadam, Chennai, and a series of inland container depots covering the major industrial corridors. Combined Indian throughput exceeds 6.5 million TEU and is growing in the mid-single-digits even at scale.

The 2025 announcement of the India-Middle East-Europe Economic Corridor (IMEC) — connecting Indian ports through the UAE, Saudi Arabia, Israel, and onward to Greek and Italian ports — sits squarely in DP World’s commercial sweet spot. The company already operates terminals at every major node along the proposed route. If IMEC reaches meaningful operational scale by 2030, DP World will be one of the largest commercial beneficiaries. Bloomberg’s logistics coverage has flagged IMEC as a strategic priority for the company.

The India growth is also paired with the company’s South Asia logistics platform expansion. New rail-linked inland container depots at Faridabad, Ludhiana, and Hyderabad allow DP World to compete for the entire end-to-end logistics chain inland from the coastal ports — not just the maritime handling fee. That is a deliberate margin upgrade strategy, and one that has been replicated in Africa and Latin America with mixed success.

The Financial Picture

DP World’s financial reporting since the 2020 take-private has been less granular than during the listed period, but the company continues to issue audited annual reports and bond-prospectus financials that allow a reasonable picture. The 2024 figures showed revenue of approximately $19.5 billion, adjusted EBITDA of around $5.3 billion (an EBITDA margin of approximately 27 percent), and net debt of around $19.0 billion against tangible equity of approximately $11.5 billion. The 2025 figures are not yet final, but are expected to show revenue in the $20.5-21.5 billion range and adjusted EBITDA in the $5.5-5.9 billion range, lifted by a return of Red Sea-Suez volumes after the disruption-driven 2024 weakness.

| Year | Revenue (USD bn) | Adj. EBITDA (USD bn) | EBITDA margin | TEU handled (m) |

|---|---|---|---|---|

| 2019 (pre-COVID) | 7.7 | 2.8 | 36% | 71 |

| 2020 | 9.6 | 3.4 | 35% | 71 |

| 2021 | 10.8 | 3.6 | 33% | 78 |

| 2022 (Imperial deal) | 17.1 | 4.9 | 29% | 83 |

| 2023 | 18.3 | 5.1 | 28% | 87 |

| 2024 (Red Sea disruption) | 19.5 | 5.3 | 27% | 88 |

| 2025E | ~21.0 | ~5.7 | ~27% | ~91 |

The margin compression from 36 percent in 2019 to 27 percent in 2024 deserves explanation. It reflects two structural shifts: the absorption of lower-margin freight forwarding and contract logistics businesses (Imperial, Syncreon) into the consolidated revenue base, and increased capex amortisation on the new African and South Asian terminals that have not yet reached full utilisation. Underlying terminal margin has stayed broadly stable. As the new terminals ramp, EBITDA margin should stabilise in the high-20s through 2026-2028.

The Red Sea Effect

The Houthi-led disruption of Red Sea shipping that intensified between late 2023 and late 2024 created the most material shock to DP World’s near-term economics in a decade. With Suez Canal volumes dropping by more than 50 percent at the peak as carriers rerouted around the Cape of Good Hope, Jebel Ali transshipment volumes for European-bound cargo fell sharply through the first half of 2024 before partial recovery in late 2024 and full normalisation through 2025.

The strategic implications are still being processed. Rerouted Asia-Europe traffic shifted some volume away from DP World’s Mediterranean and Red Sea hubs (notably Sokhna and the Suez transshipment business) and toward southern African ports — favourable for DP World’s South African operations but unfavourable for the Egyptian terminals. The disruption also accelerated multinational discussions about supply-chain resilience and corridor diversification, including increased commercial interest in IMEC and in alternative trans-Eurasian rail routes via central Asia. For deep context on the regional energy implications, see our coverage of Qatar’s LNG expansion, which faces similar Red Sea routing decisions.

Comparison with Global Peers

Five operators dominate the global container terminal industry. Comparing them clarifies what is unique about DP World.

| Operator | Annual TEU (m) | Marine terminals | Ownership type | Strategic profile |

|---|---|---|---|---|

| PSA International (Singapore) | 97 | ~50 | Singapore SWF | Asia-centric, deep concessions |

| DP World | ~90 | 82 | Dubai government | Global, integrated logistics |

| Hutchison Ports (CK Hutchison) | ~85 | 53 | Listed Hong Kong | Asia-Europe focus |

| APM Terminals (Maersk) | ~75 | 59 | Listed Maersk subsidiary | Maersk-anchored |

| China COSCO Shipping Ports | ~140 (incl. minority) | 50+ | Chinese state | BRI-aligned global |

PSA leads on raw throughput because of Singapore’s 39-million-TEU domestic transshipment scale. DP World leads on geographic breadth and on integration with adjacent free zone, customs, and trade-finance functions. Hutchison and APM Terminals are increasingly facing structural pressure as their parent companies consolidate around different strategic priorities — Hutchison’s January 2025 announcement of selling 43 ports outside China to a BlackRock-MSC consortium for $22.8 billion, reported by Bloomberg, marked one of the largest port industry transactions in history and removed a major DP World competitor in important Latin American and European markets.

The Hutchison-MSC deal also reframes the competitive landscape. MSC, already the world’s largest container shipping line, is now becoming one of the world’s largest terminal operators. That vertical integration could pressure DP World’s relationships with shipping lines, who may prefer MSC-controlled terminals when scheduling Mediterranean-Asia routes. DP World’s response will likely include deeper anchor partnerships with the remaining major shipping lines — particularly Maersk, CMA CGM, and Hapag-Lloyd — and accelerated investment in geographies where MSC’s terminal control is weakest.

Investor Angles

DP World was taken private by Port and Free Zone World in February 2020 in a transaction valuing the equity at approximately $13.9 billion. Public equity exposure to the company is therefore not directly available. However, several adjacent vehicles provide useful indirect exposure:

DP World listed bonds. The company maintains an active bond and sukuk programme, with multiple lines listed on Nasdaq Dubai, the London Stock Exchange, and the Singapore Exchange. Yields run 100-160 basis points over US Treasuries depending on maturity, reflecting an investment-grade Baa2/BBB profile from Moody’s and S&P respectively. Bond investors get a credit-grade exposure to the global terminal portfolio.

A.P. Moller Maersk (CPH:MAERSK-B). Maersk is DP World’s single largest commercial counterparty as a shipping line, with terminal usage agreements at most major DP World hubs. Maersk equity therefore offers indirect exposure to global trade flows, including DP World terminal utilisation.

Indian listed terminals. Mumbai-Pipavav is partially listed, providing direct exposure to that specific DP World concession. Other Indian listed terminals (Adani Ports, JSW Infrastructure) do not overlap with DP World but offer comparable industry exposure.

Saudi PIF holdings. The Public Investment Fund holds adjacent logistics-platform investments through its 2024-2025 strategy, complementing DP World’s regional cooperation rather than competing with it. See our Saudi PIF portfolio deep dive for the broader picture.

The 2026 Strategic Agenda

Three big initiatives define DP World’s 2026 strategic agenda:

Digital logistics platform completion. The company has been building a unified end-to-end trade platform — initially branded as DP World Logistics, now positioned as the firm’s broader digital backbone — that handles documentation, customs, freight forwarding, and finance integration across the entire DP World network. The platform is functionally a successor to the abandoned TradeLens initiative that Maersk-IBM closed in 2022, except that it is anchored to a single terminal operator’s network rather than industry-wide. Commercial rollout has been gradual, with full deployment now targeted for late 2026.

Port electrification and green bunkering. All major DP World terminals are committed to electric quay-crane operations and to providing green-fuel bunkering (methanol, ammonia) at a subset of strategic locations by 2028. Jebel Ali, London Gateway, and Sokhna are targeted as the lead electrification hubs. The Financial Times has reported that the capex commitment runs into single-digit billions across the network through 2030.

Africa and India corridor deepening. The 2026 capital plan front-loads investment in Berbera, Sokhna, Dakar, Mumbai-Pipavav, and several inland logistics platforms across both continents. Imperial Logistics integration will continue, with deeper warehouse and freight-forwarding cross-sell into existing DP World maritime customers. The financial impact should appear in 2027-2028 results as the new capacity ramps.

The Energy and Trade Linkage

DP World does not handle bulk energy commodities directly — Jebel Ali is a container port, not a crude or LNG terminal — but the company sits at the heart of the trade flow that energy producers depend on. Saudi product exports, Iraqi container traffic, UAE manufacturing exports, and inbound consumer goods all pass through DP World terminals. The relationship between regional oil revenues and DP World volumes is therefore tighter than the company’s pure container-port classification suggests.

For deeper analysis on how energy demand patterns interact with regional trade, our global oil demand 2030 forecast analysis provides the broader macro context. The forecast trajectories for oil demand also drive the trade volumes that DP World captures — particularly through the Asia-Europe corridor that links Asian manufactured exports to Middle Eastern oil revenue.

Risks and Watch Items

Three risk vectors warrant ongoing monitoring through 2026:

Geopolitical disruption to specific corridors. The Red Sea-Suez disruption in 2024 demonstrated how quickly volumes can move away from DP World hubs. Future disruptions in any major corridor — Hormuz, Malacca, or the Mediterranean — would have similar effects.

Counterparty consolidation among shipping lines. The Hutchison-MSC deal accelerates the integration trend among the largest shipping lines. If MSC, Maersk, or CMA CGM acquire additional terminal capacity, DP World’s bargaining position with those carriers could weaken.

Capital-discipline trade-off. The accumulated capex programme of the past five years has lifted net debt to elevated levels. Maintaining the EBITDA margin trajectory while continuing to deploy capital in Africa and India will require careful project selection. Bond markets have already signalled they expect leverage to start trending downward in 2026.

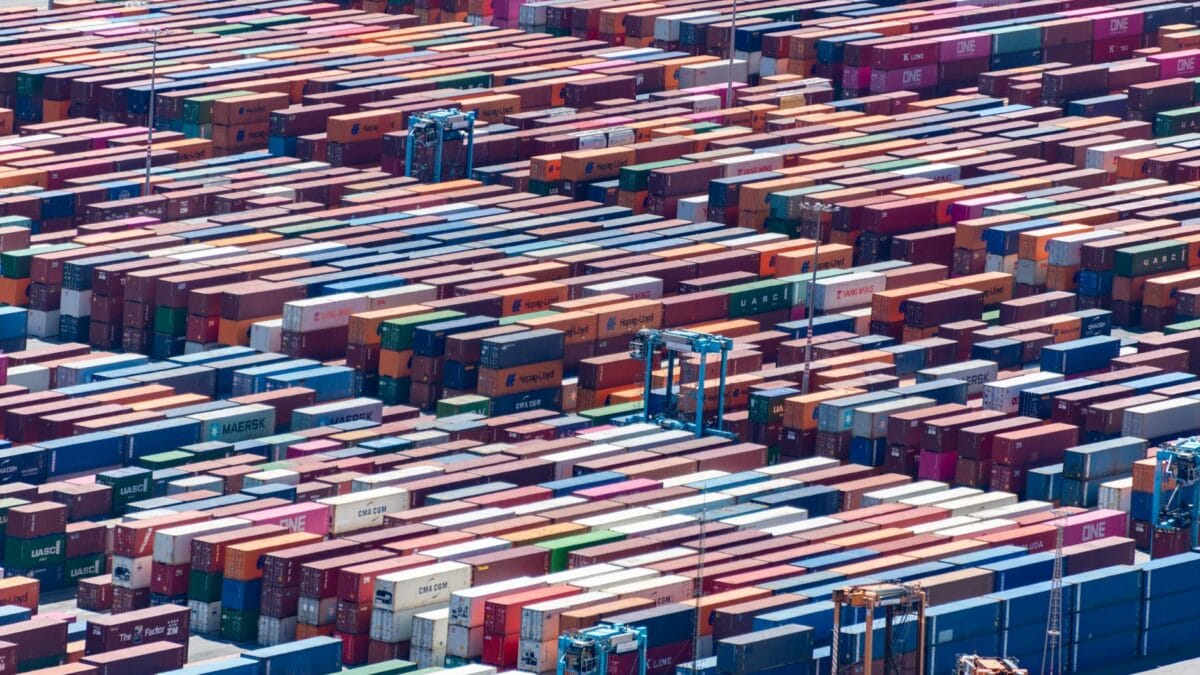

How DP World Operates a Terminal: The Mechanics

Most readers never see the inside of a working container terminal. Understanding the mechanics matters because it explains why DP World can charge what it charges and why margins are reasonably defensible against pure low-cost competition. A modern container terminal is a tightly choreographed industrial system in which every minute of crane idle time has a measurable cost. At Jebel Ali, the four operating terminals together field 67 quay cranes, more than 200 rubber-tyred gantry cranes for yard handling, and a fleet of straddle carriers and terminal tractors that move containers between the quay and the storage yard.

The commercial economics work like this. Shipping lines pay terminal handling charges per container — typically in the range of $130 to $260 per TEU at major DP World hubs, depending on volume commitments and the specific contract. The terminal earns roughly that amount once on the way in and a separate fee on the way out. Storage charges accrue if containers stay in the yard beyond the free-time period, which is typically four to seven days at the contracted volume tiers. Add in stevedoring, intra-yard movements, container weighing, customs lodgement fees, and value-added warehousing, and a single TEU can generate $200 to $450 of revenue across its full passage through a major DP World terminal.

The cost side is dominated by labour, energy, equipment depreciation, and concession fees to the host state. Productivity is therefore the single most important operating metric. Top-tier DP World terminals achieve crane productivity of 30 to 36 moves per hour per crane on the largest vessels, against industry averages closer to 24 to 28. That productivity premium is partly equipment-driven and partly the result of integration with the digital scheduling layer that the company has been building.

The People Side: Workforce and Localisation

DP World employs approximately 105,000 people globally as of the start of 2026, up from roughly 56,000 before the Imperial Logistics integration in 2022. The workforce is heavily skewed toward operational roles — terminal operators, crane operators, freight forwarders, customs clerks — with corporate functions concentrated in Dubai, London, and Johannesburg.

The UAE workforce of approximately 9,000 includes a meaningful Emirati cohort under the country’s Tawteen localisation programme. The pace of Emiratisation at DP World specifically has been a discussion point in Dubai economic policy circles, with the company adding several hundred Emirati nationals annually since 2022. Most are concentrated in middle-management, terminal operations supervisor, and corporate services roles rather than entry-level positions, which remain dominated by South Asian expatriate labour.

The Saudi Cooperation Angle

The DP World-Saudi cooperation track deserves specific mention because it has accelerated meaningfully through 2024-2025. DP World now operates the King Abdullah Port Sokhna concession in Egypt, which serves Saudi-bound transhipment volumes, and has signed extended logistics platform cooperation agreements with several Saudi entities including Aramco’s logistics arm and the Saudi Ports Authority. The cooperation falls short of direct DP World concession ownership inside Saudi Arabia — the kingdom continues to operate its major ports through Saudi Arabian authorities and through specialised concessionaires — but the operational coordination is materially deeper than what a textbook reading of the two governance structures would suggest.

One specific 2025 milestone was the signing of a memorandum of understanding between DP World and Saudi authorities on cross-border supply-chain digitisation, allowing customs documentation to flow seamlessly between Jebel Ali, Sokhna, and Saudi inland destinations. The practical commercial impact is the elimination of several hours of paperwork-driven delay per cross-border shipment, which compounds across the millions of TEU moving annually between UAE-Egypt-Saudi corridors.

What to Watch in the Q1 and H1 2026 Numbers

For analysts and observers, three specific data points in the upcoming half-year disclosures will indicate whether the strategic agenda is delivering:

Suez transit recovery. The percentage of Suez Canal volumes restored to pre-disruption levels — and how that flows into Sokhna and Mediterranean DP World terminals — is the single most important volume indicator for 2026.

Africa segment EBITDA. Imperial Logistics integration has been complex. Investors are watching whether the African segment crosses into double-digit EBITDA-margin territory in the H1 2026 numbers, signalling that the Imperial integration costs are receding.

Bond market signals. DP World’s outstanding sukuk and conventional bonds trade actively. A tightening of credit spreads versus Saudi sovereign and Dubai sovereign would indicate that the market is buying into the deleveraging trajectory the company has signalled.

Together, these three data points will tell observers whether the 2026 strategic agenda is on track or whether near-term complications — Red Sea, Hutchison-MSC, capital discipline — are constraining the trajectory more than headline messaging suggests.

The Bottom Line

DP World in 2026 is one of the most integrated, geographically broad, and strategically valuable logistics operators in the world. The combination of a state-backed ownership structure, a 50-year operational track record, $20-billion-plus revenue base, and exposure to nearly every major shipping corridor places the company in a small peer set with PSA International, COSCO, Hutchison, and APM Terminals. None of those peers replicates DP World’s specific blend of state integration plus global breadth plus end-to-end logistics ambition.

The next two years will test whether the strategic agenda — digital platform, electrification, Africa-India corridor expansion — translates into the next leg of margin and volume growth, or whether the post-2020 take-private leverage and the post-2024 Red Sea complications constrain the trajectory. Either way, DP World’s Jebel Ali anchor remains one of the single most valuable infrastructure assets in the Middle East, and the company’s footprint will continue to define how a meaningful share of global trade actually moves through 2030.

For business leaders, regional analysts, and capital allocators, the conclusion is straightforward: DP World is not a passive port operator. It is a strategic instrument of Dubai’s economic policy, a structural beneficiary of Africa-India growth, and one of the few logistics platforms with the scale to navigate whatever supply-chain reconfiguration the next decade brings.